Overview

The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, created a new category of tax-advantaged account for children, commonly known as "Trump Accounts." Account elections can be filed now on Form 4547; contributions are permitted beginning July 4, 2026. This guide addresses the questions we hear most often from families.

How Do You Open the Account?

- Before you start | Reference the latest information on the official Trump Account website: Trump Accounts - Jumpstarting the American Dream. Details have been evolving continuously, so any written instructions could be outdated.

- Step 1 | File Form 4547: Go to Trump Accounts | Internal Revenue Service, and file Form 4547 online without filing or amending a tax return. If the child was born between January 1, 2025, and December 31, 2028, check the box in Part III of Form 4547 to claim the one-time $1,000 pilot program deposit. Note: For an eligible child to receive a $1,000 pilot program contribution, an election for a pilot program contribution must be filed by an individual who anticipates that the child will be his or her qualifying child for the year in which the election is made, typically a parent or guardian.

- Step 2 | Wait for a Treasury confirmation email: After IRS processing, the Treasury will send an email with account activation instructions.

- Step 3 | Download the official Trump Accounts app: Available on the App Store and Google Play. The app is required to complete account setup.

- Step 4 | Complete activation in the app: Follow the prompts to finalize the account. The $1,000 deposit is deposited directly into the child's account; it is not a refund or a check to you.

Who Qualifies?

The child (beneficiary) must meet all of the following requirements:- Must be a U.S. citizen.

- Must have a valid Social Security number before the account election is filed.

- Must be under age 18 at the end of the calendar year in which the election is made.

- Only one funded Trump Account is permitted per child at any time.

Who May Open and Manage the Account?

- A parent or legal guardian may open and manage the account on behalf of the child.

- Grandparents and adult siblings will also be permitted to open an account for a minor who does not already have one.

- An account may be opened without an immediate contribution to claim the government seed contribution of $1,000.

Who Can Contribute, and How Much?

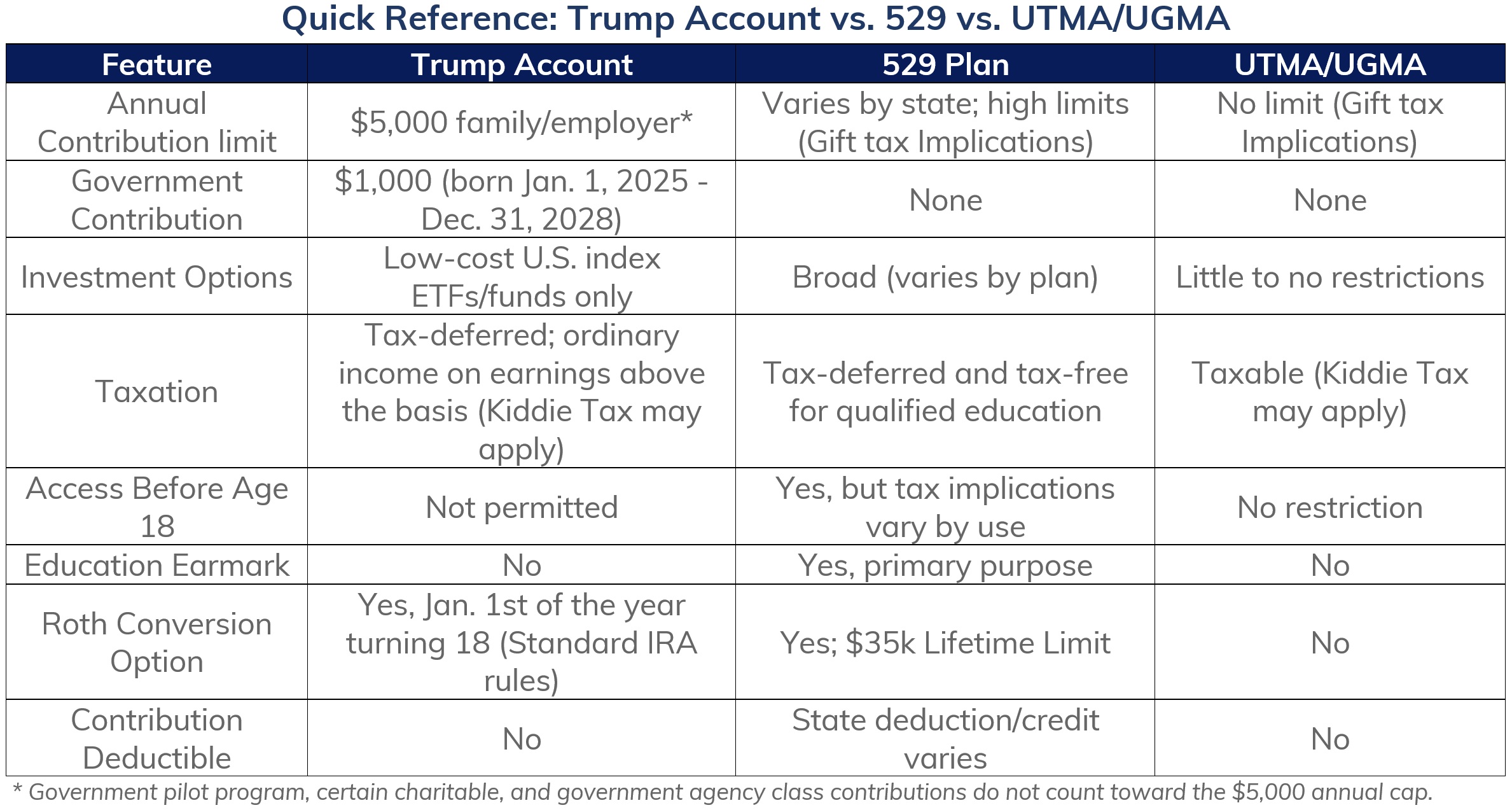

Annual contribution cap: $5,000 in aggregate "counted" contributions per year per child with no earned income requirement to allow immediate contributions for newborns.

Contributions that count toward the $5,000 cap:

- Parents, the account beneficiary, grandparents, and any other individual. Employer contributions are limited to $2,500 per year and count toward the $5,000 combined cap.

Contributions that do NOT count toward the $5,000 cap:

- Federal government $1,000 pilot program deposit (children born 2025–2028), state and local government contributions, and those made broadly by charitable organizations.

Example:

In 2026, parents contribute $2,000, and the employer contributes $1,000. The pilot program also deposits $1,000. The $3,000 in family/employer contributions consumes $3,000 of the $5,000 cap, leaving $2,000 available for a grandparent to contribute. The $1,000 pilot program deposit does not reduce the remaining cap.

Note: It is currently uncertain whether contributions to a Trump Account qualify for the annual federal gift tax exclusion. Treasury guidance on this point is pending.

What Investments Are Allowed?

During the growth period (from account opening through December 31 of the year the child turns 17):- Only Treasury-designated "eligible investments" are permitted.

- Eligible investments must: (a) track an index of primarily U.S. companies, (b) not use leverage, and (c) charge annual fees of 0.10% or less. In practice, this means broad U.S. equity index mutual funds or ETFs from low-cost providers.

After the growth period ends (January 1 of the year the child turns 18):

- The account transitions to a traditional IRA, and the full range of IRA-eligible investments becomes available.

What Happens After the Child Turns 18?

- Starting on January 1 of the year the beneficiary turns 18, the growth period has ended, and the account is treated similarly to a traditional IRA.

- The account is now legally governed by Traditional IRA rules. The mechanics of the transition into a Traditional IRA may be handled by the Custodial Agreement for such accounts, in most cases, automatically. Once the account is officially a Traditional IRA, the beneficiary may transfer it to any IRA provider of their choice.

- SEP and SIMPLE contributions may not be made to the account post-conversion.

What Are the Tax Implications?

Contributions:- Made with after-tax dollars, meaning no deduction is available.

- Earnings grow tax-deferred throughout the growth period.

Basis Tracking:

- Contributions from family members and the beneficiary create tax basis, reducing the taxable amount of future Roth Conversions.

- Contributions from Treasury (pilot program), employers, government agencies, and charities do not create basis. Those amounts will be fully taxable upon withdrawal. The IRS has released draft Form 5498-TA, which will require the account custodian to annually report the account’s basis, helping simplify long-term basis tracking for families.

- The account is not aggregated with other Traditional IRAs for the pro rata rule, applicable for Roth Conversions, during the growth phase, i.e., before it is converted into a regular IRA.

Withdrawals:

- No distributions are permitted during the growth period (except trustee-to-trustee transfers or return of excess contributions).

- After age 18, distributions are taxed as ordinary income, consistent with traditional IRA rules. Since most contributions contribute to basis, only the earnings are considered taxable income, similar to an IRA with non-deductible contributions.

Death:

- Child dies before January 1 of the year they turn 18 (growth period): the account terminates, and proceeds pass to the estate or a named recipient. The fair market value of the assets on the date of death, reduced by basis, is treated as ordinary income (not capital gains).

- Child dies on or after January 1 of the year they turn 18 (post-growth period): The account becomes an inherited IRA and follows the standard RMD rules for inherited accounts.

Planning Angles to Consider

- Capture the free $1,000: For children born 2025–2028, filing Form 4547 and checking Part III secures a free $1,000 deposit.

- Roth conversions: Starting on January 1 of the year the beneficiary turns 18 (or after the Kiddie Tax ceases to apply), the child can convert all or part of the account to a Roth IRA. If the child is in a low tax bracket during early working years, locking in tax at that rate and allowing decades of tax-free compounding is likely the most significant planning benefit this account offers.

- A supplement to other savings, not a substitute: The $5,000 annual cap is relatively modest. Trump Accounts are best viewed as a supplement to, not a replacement for, 529 plans, UGMA/UTMA accounts, or other savings vehicles.

- Employer contributions: Employers may contribute up to $2,500 per year under a Section 128 plan. If your employer offers this benefit, the contribution does not count as current taxable income to the employee or to any dependents of the employee.

- Required minimum distributions (RMDs): After age 18, the account is subject to traditional IRA RMD rules if not converted to a Roth IRA. Though beneficiaries of these accounts will not be taking RMDs for many decades from today!

Are Transfers to Another Custodian Allowed?

- Initiating a trustee-to-trustee transfer to an alternate custodian of your choice is allowed, provided that the account is first opened through official channels and has been established for at least 1 year. July 4th, 2027, would be the earliest possible transfer date.

- Several major custodians, including Charles Schwab, will accept Trump Accounts, with final guidance on the transfer process pending. For now, we recommend opening the account through official channels and revisiting a custodian transfer once the operational procedures are clearly established.

- Unlike IRA-to-IRA rollovers, there is no 12-month waiting restriction between transfers; however, the transfer must be a direct trustee-to-trustee transfer of the entire account balance. No partial transfers are permitted.

For Additional Information and Updates, Visit:

- Official portal: Trump Account overview | Trump Accounts

- IRS guidance: Trump Accounts | Internal Revenue Service

The Woodmont Team

July 13, 2026

This document contains general information only and is not intended to be relied upon as a forecast, research, investment advice, or a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The information does not take into account any reader’s financial circumstances or risk tolerance. An assessment should be made as to whether the information is appropriate for you with regard to your objectives, financial situation, present and future needs.

The opinions expressed are of the date of publication and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by Woodmont to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to fruition. Any investments named within this material may not necessarily be held in any accounts managed by Woodmont. Reliance upon information in this material is at the sole discretion of the reader. Past performance is no guarantee of future results.