Source: Pinterest, AI creator unknown

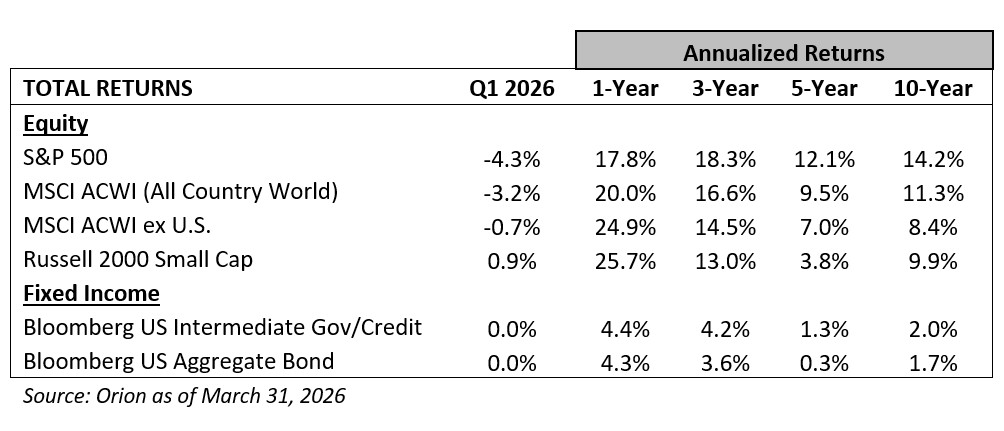

Source: Pinterest, AI creator unknownA modest consolation for diversified investors amid the instability is that the historically narrow stock market of the past few years has undergone a powerful rotation. Dividend-focused, value, and non-U.S. stocks outperformed large-capitalization growth stocks for the second consecutive quarter.

The extent of the rotation muted the declines of the All-World and S&P 500 indices (down 3% and 4%, respectively) in a quarter when the Magnificent Seven, which made up 34% of the S&P 500’s market capitalization at the start of the year, fell 11%. Moreover, investors who remained leery of popular Wall Street private credit income strategies, which borrow money to boost the yields of already highly leveraged loans, had a much calmer quarter than any peers who chased those yields. For context, one need only note the gates restricting investor fund redemptions and the 20% to 40% first-quarter stock price declines of Wall Street’s highest-profile private credit asset managers. Yet another reminder that when investing, “there is no free lunch.” The pursuit of higher returns means accepting more risks, and debt only magnifies those risks.

It would be difficult to address all of the quarter’s events and provide perspective on portfolio positioning in this abbreviated commentary. Please let us know if you want to dig deeper into a topic that might be dampening your optimism.

In this commentary, we will discuss current equity and bond prices and our perspectives on valuations and risks in light of the rapidly evolving landscape. We will also consider whether investors should view AI as a panacea or a cause for panic. A spoiler alert! We believe the wisdom of investor and philanthropist, John Templeton, is worth sharing, particularly given the nascent nature of AI. That is “an investor who has all the answers doesn’t even understand all the questions.”

Equities: Some Corrections, Particularly Under the Hood

The average intra-year drawdown – the decline from the high to the low - for the S&P 500 has been 14% over the last 46 years. (Source: J.P. Morgan) So, in Wall Street parlance, a “correction” happens on average every year. Down 9% from the intra-quarter high to low, the S&P 500 approached correction territory in the first quarter and reached prices last seen in August of 2025. Peaking in late February, ex-U.S. stocks slid 12% from the quarter’s highs.

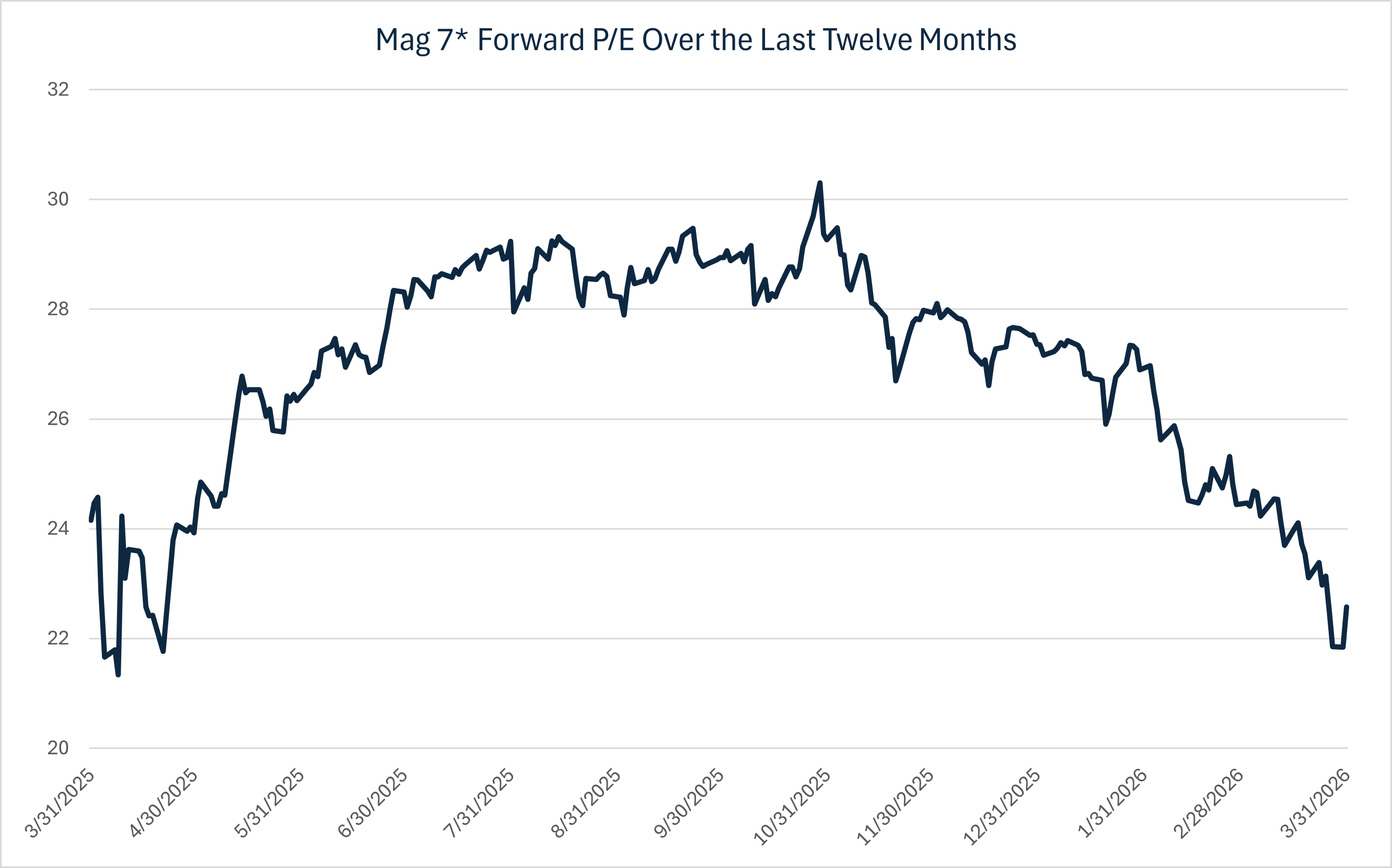

Looking under the equity index hood at sectors and styles, the first-quarter volatility was extreme in many cases. For instance, fear that AI could disrupt software business models contributed to State Street Group’s Software Services ETF falling 24% in the quarter. The Magnificent Seven toppled 16% intra-quarter. The group of closely watched stocks ended the quarter down 11% as the AI-investment focus shifted from revenue and margin expansion opportunities to the historic capital spending required to support its growth. The group now trades at 23x 2026 forward twelve-month earnings, down from over 30x in October 2025. Magnificent Seven constituent and software and cloud storage bellwether, Microsoft (MSFT), now trades at 20x forward earnings, compared to a five-year average multiple of 29x. (Source: FactSet Data Systems).

In the commodity market, precious metals continued their wild ride with gold and silver ending the quarter down 12% and 35% from their January highs. The sell-off was counter to the conventional wisdom that these metals outperform when inflation fears spike, only adding to questions surrounding the assets’ big gains in recent periods. Copper fell 9% from its January peak. Most agricultural commodity prices increased, partly due to fear that disruptions to Middle Eastern fertilizer supplies could harm crop production.

An obvious bright spot for equity performance this quarter was energy stocks, which gained 38%. These gains pushed the sector’s weight to 4% of the S&P 500. During the Great Financial Crisis, energy was approximately 15% of the index. We would not be surprised to see the sector perform well in the quarters ahead. Specifically, political and production risks in the Middle East (20% of global oil flows through the Strait of Hormuz) could lead to higher for longer oil prices and/or a premium for quality producers, who tend to benefit during periods of global supply disruption.

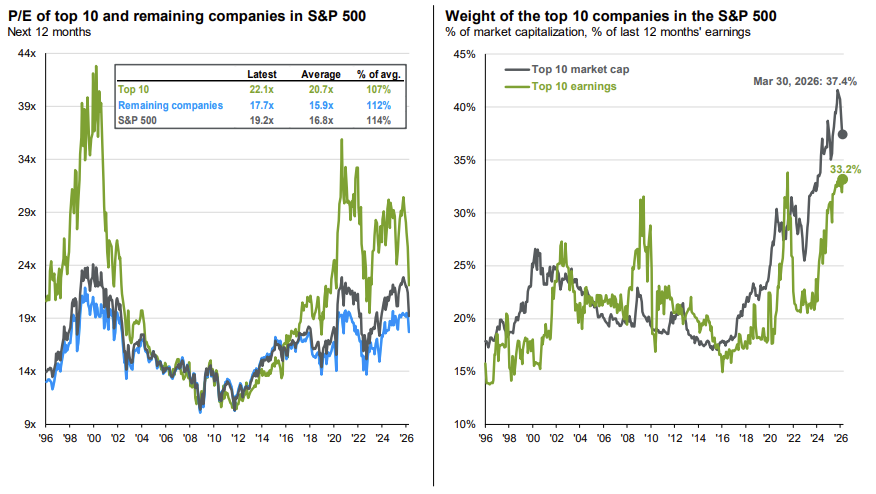

Although valuation ranges across sectors are significant, the S&P 500 and ex-U.S. indices are trading at 20x and 15x consensus 2026 earnings estimates. The S&P 500 was at 23x last fall. It would be difficult to conclude that U.S. stocks, in the aggregate, are cheap relative to historical measures. It’s a notable contraction, however, and for the first time in several quarters, many quality growth stocks trade at palatable valuations, with a few insiders purchasing shares in the open market. Source: JP Morgan “Guide to the Markets” as of March 30, 2026

Source: JP Morgan “Guide to the Markets” as of March 30, 2026Non-U.S. stocks declined 9% from their February highs, underperforming U.S. stocks since we attacked Iran. The valuation multiple for non-U.S. stocks expanded over the past 18 months, thanks in part to a weaker U.S. dollar. Additionally, the risks of higher energy prices are greater for Europe and Asia. Specifically, today’s 15x forward earnings is up from 12x in the fall of 2024, and unlike the U.S., Europe and Asia are net importers of energy (oil and LNG in particular).

Exposure to non-U.S. stocks remains an important part of a diversified portfolio and serves as an embedded hedge to the U.S. dollar. Yet, we will be measured in our portfolio weightings relative to the All-World index, which is currently about 38% non-U.S. stocks. Put simply, we believe the highest-quality and most innovative companies remain predominantly U.S.-based and, despite current global tensions, continue to successfully export their goods and services.

Economy: Oil and Recession?

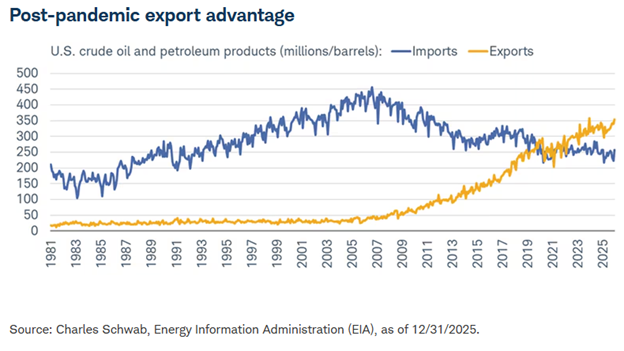

Wall Street’s 2026 robust earnings forecasts for 17% growth will be tested when companies start reporting first-quarter results and updating outlooks in the coming weeks. Goldman Sachs recently raised its recession probability over the next twelve months to 30% due to the threat of sustained higher energy prices. While the threat to consumer confidence is a risk everyone is monitoring, the U.S.’s sensitivity to an oil price spike has declined over the years. Thanks in part to the shale boom, we are a net exporter of oil and LNG, and higher prices provide a boost to energy-producing states. Also, gasoline currently accounts for a small share of personal expenditures at just 2%, and the incentive for politicians to keep prices low should not be underestimated with the November mid-term elections looming. (Source: Schwab and the Energy Information Administration)

Economy: How About Confidence and Recession?

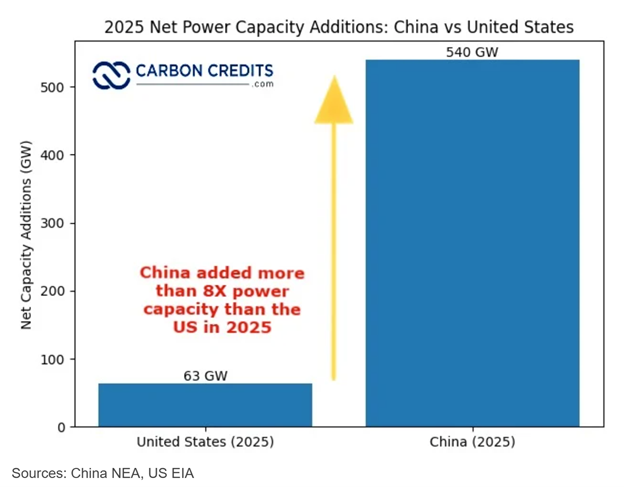

What might prove more impactful for the outlook than volatile oil and gas prices is whether the anticipated economic boost from accelerated bonus depreciation, lower taxes for many consumers, and large-scale investments (in infrastructure and R&D) related to the growing energy arms race will materialize. Of note, some estimate China has a 50% current energy price advantage over the U.S. and plans to press this advantage, investing $500 billion in grid and power plants in 2025 alone. This effort resulted in an additional 540 GW of power, while the U.S. added just 63 GW. (Source: National Energy Administration) Nvidia CEO, Jensen Huang, has been vocal about this discrepancy, noting that as part of U.S. AI development efforts “we are building chip plants, supercomputer facilities, and AI factories. They all require energy.”

Business owners and C-suite executives must be confident in the policy rules of the road when deciding to invest capital or hire new workers. Yet, most agree that the range of policy priorities – both federal and state - seems as significant as ever. We are hopeful, however, that policymakers (or at least their constituents) recognize that an environment that preserves opportunities for individual economic mobility and rewards innovation and entrepreneurial risk-taking remains crucial to the U.S.’s economic success.

Bonds: Following the Herd Can Be Dangerous

Before the U.S. attack on Iran, U.S. Treasuries reflected an 80% probability that the Federal Reserve would cut rates at least twice by year end. Today, the market is assigning a less than 2% probability for interest rate cuts. (Source: Wall Street Journal) Two and Ten-Year Treasury yields are now 3.79% and 4.30%, which is up from 3.38% and 3.97% just four weeks ago. To understand the magnitude of this move in a short period, if you bought a Ten-Year Treasury in February, you would have lost 3% in value by late March in this “risk-free” asset.

Today’s higher rates increase the appeal of owning fixed-income. We are weighing modestly increasing duration in most portfolios from our current target of 3.0 to 3.5 years. The Bloomberg U.S. Government/Credit fixed-income benchmark’s duration is 6.1. While a modest increase may be appropriate, we are not interested in matching the benchmark’s duration given the range of interest-rate outcomes in today’s environment.

As for taking more credit risks, spreads (the premium investors receive for accepting credit risks) remain historically tight. While a window of wider spreads opened last year to purchase municipal bonds for clients in the highest tax bracket, tax-equivalent yields recently fell below Treasury yields. This may reflect the anticipation of higher tax rates. Nevertheless, it is tough to accept the lower net yields and reduced liquidity characterizing the current municipal market.

The investor herd moved aggressively into private credit in the past 10 years. Specifically, the asset class grew from $300 billion in 2010 to an estimated $2 trillion today (source: Preqin). Some high-profile bankruptcies revealed initial cracks in credit quality and raised issues regarding loan underwriting last year. Yet, recent concerns about the impact of AI on software businesses, which analysts estimate represents 30% of private credit loans, have ushered in a new level of angst among many institutional and high-net worth investors drawn to the asset class’s enhanced yields and advertised lower volatility. Reaching for the 2%-3% of extra yields of recent years could prove expensive if Net Asset Values are impaired 20%-25% as many now forecast, and fund “gates” restrict investor redemptions.

If private credit values sufficiently reset to compensate investors for the inherent risks in leveraged loans, investing in the sector could prove attractive for risk-tolerant investors. Our primary filter for traditional fixed-income and alternative credit strategies remains assessing the risk of principal loss. As regular readers of this commentary know, we prefer to accept the risks of equity investments where the long-term upside from compounding returns is great, versus fixed-income, where collecting interest and the return of principal is the best you can do.

AI: Panacea or Cause for Panic?

As noted in our January commentary, AI-related capital investments reached nearly 2% of GDP in 2025. By comparison, neither the Interstate Highway nor the Apollo projects eclipsed 0.5% of GDP. While it will take time to determine if the enormous AI investments yield attractive returns, concerns about the extent to which AI could change business strategy, labor markets, and energy consumption are increasing. Some, such as Anthropic CEO, Dario Amodei’s labor displacement theories, or Citrini Research’s recent “Intelligence Crisis” memo, paint a scary picture.

“My prediction is for 50% of entry-level white-collar jobs being disrupted is 1-5 years.” Dario Amodei, CEO, Anthropic (Developer of the AI Assistant, Claude)

Others are more sanguine and liken AI’s emergence to historical technological wonders. For instance, typists, armies of tellers, and fields of farm workers found new opportunities in emerging industries. Of course, many of these jobs were later replaced, reflecting a natural cycle of innovation and economic progress.

Not all the worry is focused on the threat of job displacement. In his recent annual letter to shareholders, BlackRock’s CEO, Larry Fink, anticipates outsized benefits for companies capable of harnessing AI. In his forecast, these AI-driven gains likely accrue disproportionately to owners/shareholders. As a result, Fink is worried about the societal implications if AI upside participation is too narrow.

“Since 1989, a dollar in the U.S. stock market has grown more than 15 times the value of a dollar tied to median wages. Now AI threatens to repeat that pattern at an even larger scale—concentrating wealth among the companies and investors positioned to capture it.” Larry Fink, CEO, BlackRock

We want to approach the AI topic with humility. In fact, the John Templeton wisdom we shared earlier about recognizing when we don’t have the answers may never be more relevant.

One thing we have observed in our firm’s 25 years, and in many historical contexts, is that when forecasts are so extreme, reality is often somewhere in between. Whether this applies to a technology moving at the pace of AI is unclear. We are convinced, however, that in today’s rapidly changing landscape, young and old professionals alike must be problem solvers, communicate honestly and clearly, show up on time and often, and don’t outsource the important work to AI. Not only would outsourcing lead to cognitive decline, but AI is ultimately a tool, and we believe tools are to be utilized, not followed.

Tax Time and Free Money!

We’ve communicated with many of you leading up to the April 15th tax deadline. Whether Tennesseans are granted another year of tax filing disaster relief, given the terrible February ice storms, is uncertain and hinges partly on FEMA funding within the Department of Homeland Security. We are monitoring closely, as are the dozens of CPAs we work with and communicate regularly. For now, the best approach is to prepare as if the April 15th deadline stands, yet withhold payment until closer to the 15th. Last year, the disaster relief, which postponed the filing and tax payment deadline, was declared on April 14.

While disaster relief remains up in the air, the recently released rules for the often-discussed “Trump Accounts,” 2026 retirement savings opportunities such as Roth catch-ups and super catch-ups, and a handful of tax strategies have come into focus on the heels of the One Big Beautiful Bill Act. We covered many of those in our July 22 update last year and are available to discuss them within the context of your long-term financial plan and tax strategy.

As for the free money, the “Trump Account” deposit of $1,000 is limited to children born between January 1, 2025 and December 31, 2028. While there are some advantages to these accounts, most notably for these newborns, the broader benefit could be helping launch a new generation of investors. For young investors with earned income, we continue to encourage taking advantage of the opportunity to fund a Roth account. Although tax laws could change, the prospect of tax-free growth and tax-free withdrawals is certainly worth rotating toward, particularly when you are young.

Thank you, as always, for your continued trust and confidence. We wish you all the best for a rewarding spring season and look forward to answering your questions.

The Woodmont Team

April 2, 2026

This document contains general information only and is not intended to be relied upon as a forecast, research, investment advice, or a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The information does not take into account any reader’s financial circumstances or risk tolerance. An assessment should be made as to whether the information is appropriate for you with regard to your objectives, financial situation, present and future needs.

The opinions expressed are of the date of publication and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by Woodmont to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to fruition. Any investments named within this material may not necessarily be held in any accounts managed by Woodmont. Reliance upon information in this material is at the sole discretion of the reader. Past performance is no guarantee of future results.